Preparing Your Fintech for the Digital Euro: Identity, Consent & Onboarding

As of mid-2025, the digital Euro has entered the preparation phase led by the European Central Bank. The ECB is reviewing legislative proposals, working with technical partners, and running early tests with selected banks and fintechs to explore how the currency will function in real environments. Final decisions are expected by 2026, with release to the public likely to follow shortly after (European Central Bank, 2024; Currency Insider, 2025).

TL;DR — Key Takeaways

- The digital Euro will bring real-time identity, consent, and settlement directly into customer wallets.

- UK fintechs must prepare now to handle ECB-certified identity flows, programmable payments, and consent tracking.

- Teams across product, engineering, compliance, and support will need to redesign onboarding and verification logic.

- Early preparation reduces compliance risk, ensures future compatibility, and positions your platform for cross-border digital transactions.

- The first 6 months should focus on auditing current flows, prototyping wallet integration, and assigning digital Euro ownership internally.

The digital Euro, unlike commercial wallets like Apple Pay or PayPal, is being developed as central bank-issued money with built-in identity and programmable features. For UK fintechs, it presents a timely opportunity to rethink onboarding and consent, especially as user expectations shift towards seamless, real-time experiences supported by trusted digital wallets.

1. What Is the Digital Euro

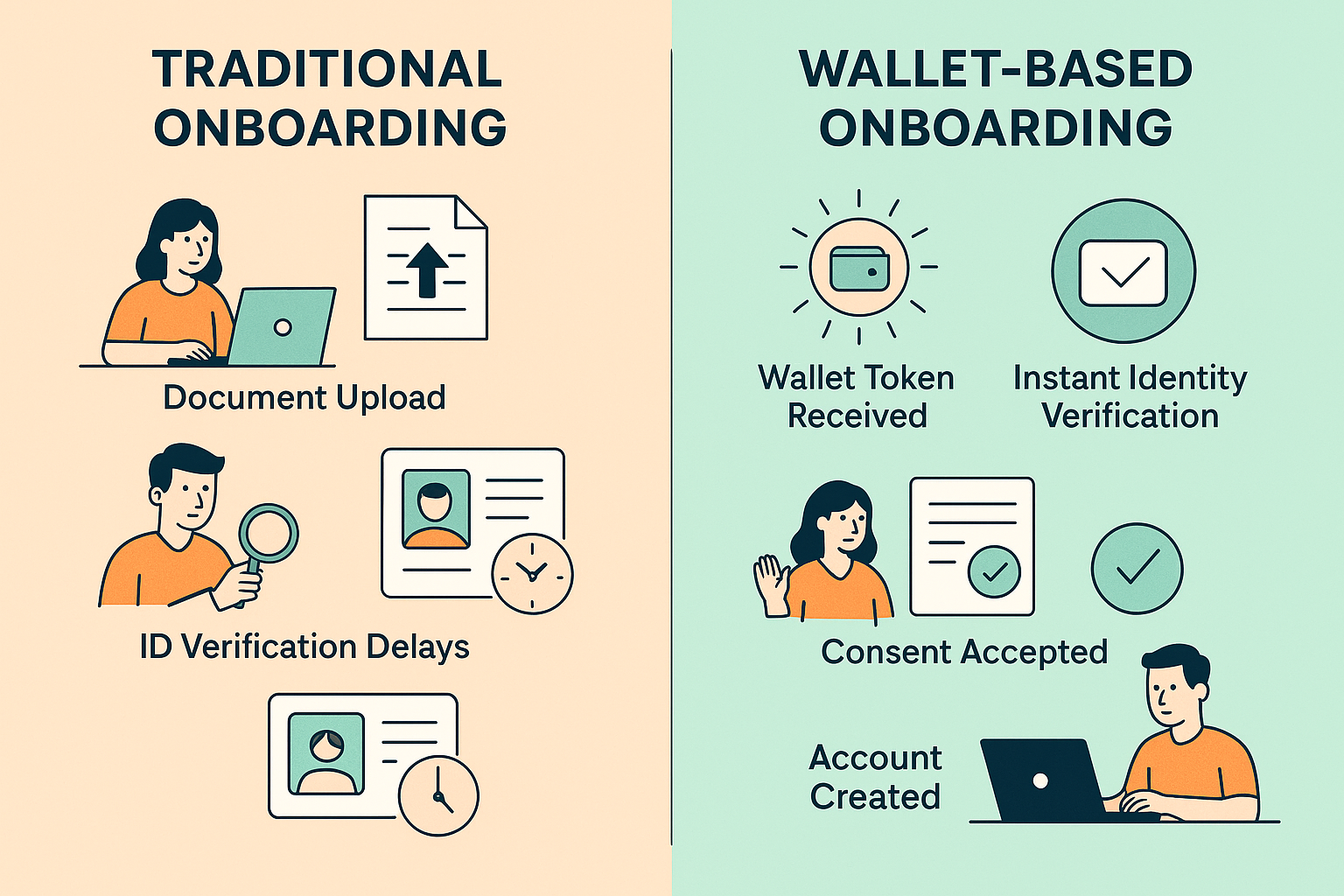

Imagine it’s 2027. A UK-based customer travels to Hamburg. They use an ECB-certified digital wallet to:

- Pay for their hotel

- Unlock a rental car with embedded ID verification

- Complete transactions instantly with no exchange fees or cross-border delays

They don’t fill out a form, scan a passport, or re-confirm their email. Everything is secure, compliant, and instant. This level of seamless experience will become normal. If your platform doesn’t support it, you risk being left out of cross-border user journeys (Reuters, 2025).

The digital Euro stands out by embedding identity, programmable logic, and real-time clearing into money itself. This changes the role of fintech infrastructure: platforms will need to process user identity and consent tokens on the fly, route compliance outcomes instantly, and shift from batch onboarding to real-time orchestration. Engineering leaders should start reviewing where current system design assumptions, such as document-based KYC or delayed settlement, may create risk under the new model, rather than relying on fintech platforms to patch these functions on top.

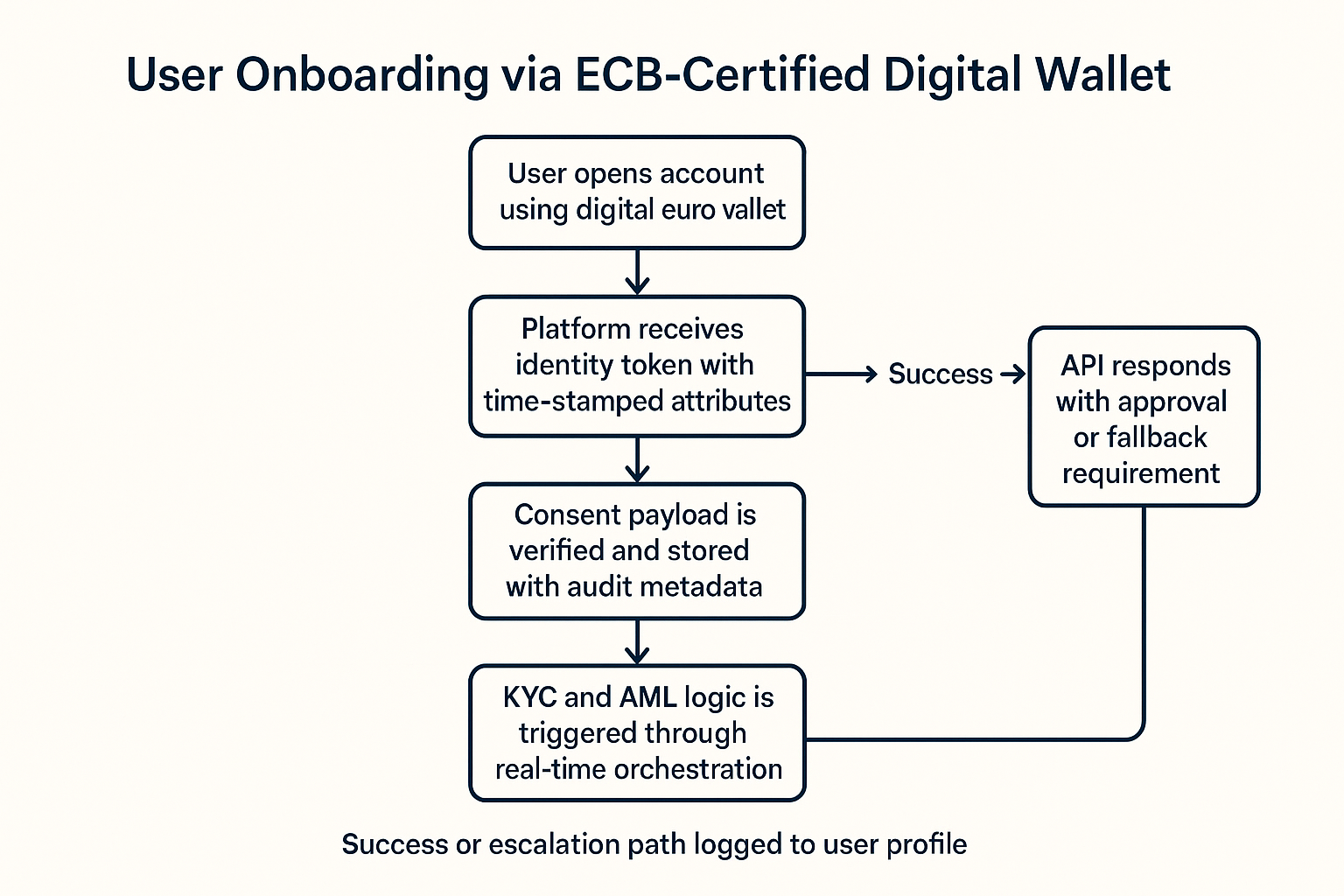

2. How the Digital Euro Will Change Sign-Up, Identity, and Consent

With the release of digital Euro wallets, customers may arrive with pre-verified identity managed by certified intermediaries. These wallets will likely provide tokenised identity and consent payloads, secure, auditable, and tied to the transaction (European Central Bank, 2025a). That means your platform must:

- Accept identity without uploading documents or scanning IDs

- Respect user consent issued via external wallets or identity hubs

- Record interactions in a traceable, privacy-compliant way

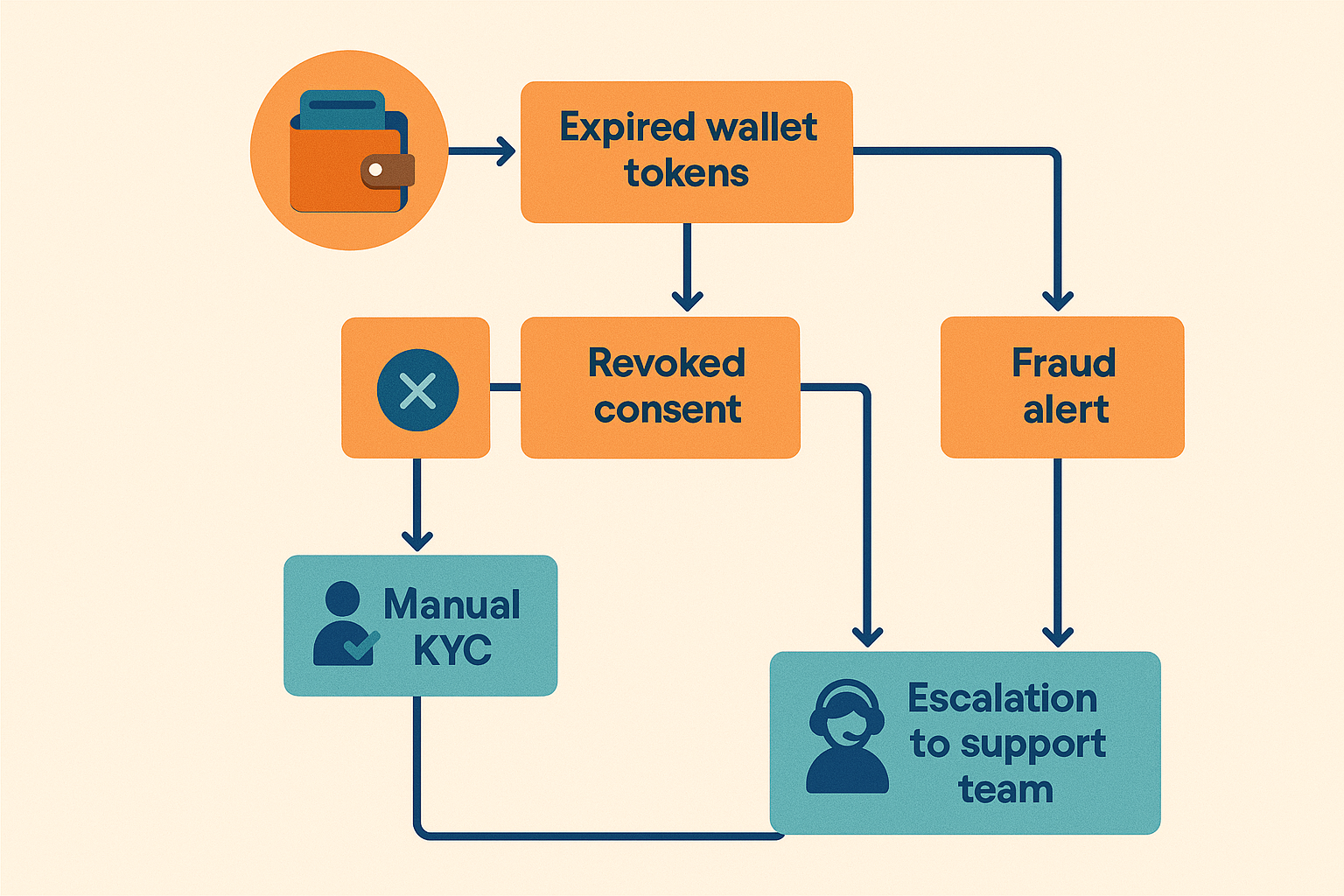

For fintechs, this is a shift from controlling the full identity flow to trusting verified sources. This introduces new challenges: how to deal with fraud cases where wallet credentials are revoked, how to trace changes in user consent, and how to deliver seamless fallback options when external systems fail. Fraud operations planning should also anticipate token anomalies, consent expiry events, and identity replay attacks. These risks require proactive detection logic and escalation paths beyond conventional fraud models. Trust will increasingly be tied to how reliably and visibly these integrations perform.

3. What to Do First in Next 6 Months

The smartest move is to prepare your systems now, while adoption is still emerging. You don’t need to rebuild everything. But you do need to clear space for new flows to be tested.

- Audit your KYC and onboarding workflows

- Check how identity data is currently verified and stored

- Map out user journeys where consent and ID are required

- Review wallet integration options (e.g. IDnow, Thales, G+D SDKs)

- Join ECB pilot/sandbox initiatives if eligible (European Central Bank, 2025b)

- Identify internal bottlenecks that would prevent wallet-based onboarding

4. What Each Team Should Start Working On (With Technical and Risk Priorities)

Digital Identity & Consent Onboarding — Functional Responsibilities

| Team | Responsibilities |

|---|---|

| Product Team |

|

| Engineering Team |

|

| Compliance & Legal |

|

| Customer Support & Experience |

|

Need Expert Help?

If internal teams are busy or unsure where to start, external experts can help.

Coder Trove supports fintechs with technical planning, digital identity integration, and prototyping wallet-ready flows. We work alongside your in-house teams so you stay in control, while moving faster.

References

- Currency Insider (2025) ECB Eyes 2026 for Digital Euro Green Light, Launch Could Follow by 2028, 17 May. Available at: https://currencyinsider.eu/ecb-digital-euro-launch-2026 (Accessed: 18 June 2025).

- European Central Bank (2024) ECB publishes second progress report on the preparation phase of a digital euro, 2 December. Available at: https://www.ecb.europa.eu/press/pr/date/2024/html/ecb.pr231204~e9e4b2cb7d.en.html (Accessed: 18 June 2025).

- European Central Bank (2025a) Digital euro scheme rulebook update, 9 April. Available at: https://www.ecb.europa.eu/paym/digital_euro/shared/files/digitaleuro-rulebook-update-2025.pdf (Accessed: 18 June 2025).

- European Central Bank (2025b) Platform of 70 market participants to test digital euro capabilities. Available at: https://www.ecb.europa.eu/paym/digital_euro/html/ecb.participants2025.en.html (Accessed: 18 June 2025).

- Reuters (2025) ECB hopes to have political deal on digital euro by early 2026, 15 May. Available at: https://www.reuters.com/markets/europe/ecb-political-agreement-digital-euro-2025-05-15 (Accessed: 18 June 2025).

- Reuters (2025) ECB hopes Trump’s crypto plan will accelerate Euro process, 6 February. Available at: https://www.reuters.com/technology/ecb-reacts-us-crypto-policy-2025-02-06 (Accessed: 18 June 2025).